IBM, to IBMers, always stood for “I’ve Been

Moved,” a reference to the way Big Blue moved employees around the country and

around the globe to get experience as they worked their way up the ranks.

Moved,” a reference to the way Big Blue moved employees around the country and

around the globe to get experience as they worked their way up the ranks.

To Wall Street, however, IBM could stand for “I’ve Been

Manipulated,” because no public company we can think of does a better job of

schmoozing Wall Street’s Finest and convincing them that there’s a there there,

when in fact the there is not quite as there as it might seem.

The quarterly earnings calls are curiously synthetic, almost antiseptic affairs, run by the CFO and focused strictly on the numbers: on the revenue number, on the cash flow number, on the share buyback number, and on the earnings number.

In particular, the per share earnings number.

The CEO never graces the call, and no actual business operators discuss their business. No success stories are told, no customers highlighted. It is all about margins and currencies and so-called one-time charges and so-called one-time gains, and tax rates, and how all those things added up to the earnings per share that quarter.

And, most especially, what that earnings per share means for The EPS Roadmap.

Manipulated,” because no public company we can think of does a better job of

schmoozing Wall Street’s Finest and convincing them that there’s a there there,

when in fact the there is not quite as there as it might seem.

The quarterly earnings calls are curiously synthetic, almost antiseptic affairs, run by the CFO and focused strictly on the numbers: on the revenue number, on the cash flow number, on the share buyback number, and on the earnings number.

In particular, the per share earnings number.

The CEO never graces the call, and no actual business operators discuss their business. No success stories are told, no customers highlighted. It is all about margins and currencies and so-called one-time charges and so-called one-time gains, and tax rates, and how all those things added up to the earnings per share that quarter.

And, most especially, what that earnings per share means for The EPS Roadmap.

But let’s back up a bit…

In May 2007 IBM held an analyst meeting to introduce a “2010 Earnings Per Share Roadmap,” to “give our

shareholders a clear understanding of the key factors driving IBM’s long-term

financial objectives.”

shareholders a clear understanding of the key factors driving IBM’s long-term

financial objectives.”

Those objectives were EPS growth of 14-16% and

EPS of $10-$11 by 2010.

EPS of $10-$11 by 2010.

To get there the company spelled out five “Key Drivers” of

the Roadmap: revenue growth, margin expansion, share repurchases, acquisitions

and retirement-related savings.

the Roadmap: revenue growth, margin expansion, share repurchases, acquisitions

and retirement-related savings.

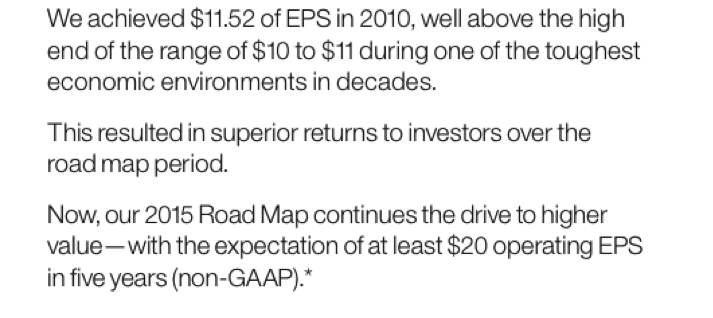

And certainly IBM got there: in the 2010 annual

report, IBM could proudly state that EPS had come in at $11.52—above the high

end of the “Roadmap” range.

report, IBM could proudly state that EPS had come in at $11.52—above the high

end of the “Roadmap” range.

And Wall

Street loves companies that beat the

high end of anything.

Street loves companies that beat the

high end of anything.

Now, it is true that the “revenue growth”

piece of the Roadmap didn’t play out as perhaps many had expected: 2010 revenues

were only 1% above 2007, the year the Roadmap was laid out.

piece of the Roadmap didn’t play out as perhaps many had expected: 2010 revenues

were only 1% above 2007, the year the Roadmap was laid out.

But the

margin expansion and cost savings played out in spades: from that $1

billion in extra annual revenue sprang added gross profits, added operating profits, and added net income of $ 4 billion each, give or take (mostly give).

margin expansion and cost savings played out in spades: from that $1

billion in extra annual revenue sprang added gross profits, added operating profits, and added net income of $ 4 billion each, give or take (mostly give).

Meanwhile, ample share repurchases acted like

gasoline on the fire, juicing EPS almost 60% on that tiny 1% revenue gain.

gasoline on the fire, juicing EPS almost 60% on that tiny 1% revenue gain.

So well did the 2010 “Roadmap” go over with shareholders and Wall Street alike, that IBM rolled out another: the 2015 Roadmap, comprising, in this order, “$8

billion of productivity improvement” (e.g. layoffs and reorgs); $50 billion in

share repurchases and $20 billion in dividends; and “four growth priorities”

that included emerging markets hitting 30% of revenue in 2015, business

analytics (e.g. Watson, the Jeopardy champ) hitting $16 billion of revenue in

2015, cloud computing hitting $7 billion of revenue in 2015, and what IBM calls

“building a smarter planet”—what everyone else calls “the internet of

everything”—hitting $10 billion of revenue in 2015.

billion of productivity improvement” (e.g. layoffs and reorgs); $50 billion in

share repurchases and $20 billion in dividends; and “four growth priorities”

that included emerging markets hitting 30% of revenue in 2015, business

analytics (e.g. Watson, the Jeopardy champ) hitting $16 billion of revenue in

2015, cloud computing hitting $7 billion of revenue in 2015, and what IBM calls

“building a smarter planet”—what everyone else calls “the internet of

everything”—hitting $10 billion of revenue in 2015.

The bottom line of all this? $20 in earnings per share by 2015.

But that target came with an asterisk,

literally:

literally:

The asterisk mentioned that the $20 target was a so-called

“non-GAAP” EPS target, which “excludes acquisition-related and non-operating

retirement-related charges.”

“non-GAAP” EPS target, which “excludes acquisition-related and non-operating

retirement-related charges.”

As we pointed out many times in these virtual

pages during the many occasions we poked fun at Hewlett-Packard before that

company, as a friend likes to say, hit the trees with no flaps down, “non-GAAP” means earnings not prepared in

accordance with generally accepted accounting principles.

pages during the many occasions we poked fun at Hewlett-Packard before that

company, as a friend likes to say, hit the trees with no flaps down, “non-GAAP” means earnings not prepared in

accordance with generally accepted accounting principles.

IBM’s 2010 “Roadmap” had come with no such

asterisk.

asterisk.

Nevertheless, IBM’s recently retired CFO, a

key driver behind both “Roadmaps,” always said the $20 EPS target was “all-in,”

i.e. while it included gains on sales of things, it also included losses on charges of things.

key driver behind both “Roadmaps,” always said the $20 EPS target was “all-in,”

i.e. while it included gains on sales of things, it also included losses on charges of things.

Fortunately—and quite remarkably, the casual

observer might think—those gains and charges on things at times almost exactly offset each other.

observer might think—those gains and charges on things at times almost exactly offset each other.

In the first quarter of 2009, the company had

a $265 million “workforce rebalancing charge” offset by a $298 million gain

on an asset sale.

a $265 million “workforce rebalancing charge” offset by a $298 million gain

on an asset sale.

And in the first quarter of 2010, another

“workforce rebalancing charge”—this time $560 million—was paired with another

one-time gain of $591 million.

“workforce rebalancing charge”—this time $560 million—was paired with another

one-time gain of $591 million.

Neat, right?

So adept has IBM been at matching the cost of

downsizing its operations with gains on sales of bits of those operations that

it was apparently hoping to generate a big enough gain from the sale of its

server business to offset the $1 billion “workforce rebalancing charge” it took in 2013 (these charges are one of the bigger growth items in IBM’s

P&L)—but Lenovo appeared to play hardball and the sale didn’t happen in

2013. Meanwhile, a different, smaller sale (at a reported measly 5-times EBITA), of a

service business to Synnex, didn’t close in time to help the 2013 EPS.

downsizing its operations with gains on sales of bits of those operations that

it was apparently hoping to generate a big enough gain from the sale of its

server business to offset the $1 billion “workforce rebalancing charge” it took in 2013 (these charges are one of the bigger growth items in IBM’s

P&L)—but Lenovo appeared to play hardball and the sale didn’t happen in

2013. Meanwhile, a different, smaller sale (at a reported measly 5-times EBITA), of a

service business to Synnex, didn’t close in time to help the 2013 EPS.

Nevertheless, IBM today proudly announced that

it had “delivered” fourth quarter EPS of $6.13 a share, “up 14% year-to-year”

to bring the full 2013 EPS to $16.28, magically in line with Wall Street’s

Finest, and right down the middle of the all-important Roadmap.

it had “delivered” fourth quarter EPS of $6.13 a share, “up 14% year-to-year”

to bring the full 2013 EPS to $16.28, magically in line with Wall Street’s

Finest, and right down the middle of the all-important Roadmap.

How it got there, though, was way more complicated.

After all, revenue dropped 5% (down 3% adjusted for

currency). Asia-Pacific revenue was down

6%. China revenue was down 23%. Pretax income dropped 8%. Pretax margins were likewise down. Free cash flow was down 13% in the quarter and 21%

for the year.

currency). Asia-Pacific revenue was down

6%. China revenue was down 23%. Pretax income dropped 8%. Pretax margins were likewise down. Free cash flow was down 13% in the quarter and 21%

for the year.

Yes, you read that correctly: free cash flow was down 21% for the year.

Oh, and the company

guided first quarter 2014 EPS to something around $2.50 a share versus Wall

Street expectations of $3.27 a share—a 24% miss.

guided first quarter 2014 EPS to something around $2.50 a share versus Wall

Street expectations of $3.27 a share—a 24% miss.

How, then, did IBM show “up 14% year-to-year”

profits in Q4 2013?

And how did the new IBM CFO manage to re-affirm the all-important, almighty $20 EPS Roadmap?

profits in Q4 2013?

And how did the new IBM CFO manage to re-affirm the all-important, almighty $20 EPS Roadmap?

Well, with a mere 11.2% tax rate, all

targets are possible, profitability-wise.

targets are possible, profitability-wise.

“But wait a minute,” the reasonably informed observer might ask. “What is really going on here? Economies are recovering around the

world. Europe had a near-death

experience two years ago and is healing. China is growing nearly 8%, not shrinking 23%. American industry is recovering broadly.

Our banks are healthier than they have been in a decade. State budgets have revived and governments are spending again.

world. Europe had a near-death

experience two years ago and is healing. China is growing nearly 8%, not shrinking 23%. American industry is recovering broadly.

Our banks are healthier than they have been in a decade. State budgets have revived and governments are spending again.

“So why the punk revenues at one of the largest, most important purveyors of IT equipment, software and services in that very same world?

“And why are ‘workforce rebalancing charges’ growing from $440 million in 2011 to $803 million in 2012 to $1 billion in

2013, even as US unemployment drops and companies from Google to Amazon to eBay

to Apple to Facebook to Salesforce can’t hire engineers fast enough?”

2013, even as US unemployment drops and companies from Google to Amazon to eBay

to Apple to Facebook to Salesforce can’t hire engineers fast enough?”

Well, IBM blames hardware, but IBM’s software

revenues were only up “3% to 4%,” and that includes acquisitions: the “all-in” approach taken by the CFO means that, unlike most companies playing the non-GAAP game, IBM does not provide organic, non-acquisition-inflated revenues. That is 3-4% growth, inflated by acquisitions, in a world where Salesforce.com is growing 35% a

year organically, and Amazon Web Services is growing…don’t ask.

Meanwhile, the rest of IBM’s business, a mix of

consulting and outsourcing, has been fair-to-middling-to-poor.

revenues were only up “3% to 4%,” and that includes acquisitions: the “all-in” approach taken by the CFO means that, unlike most companies playing the non-GAAP game, IBM does not provide organic, non-acquisition-inflated revenues. That is 3-4% growth, inflated by acquisitions, in a world where Salesforce.com is growing 35% a

year organically, and Amazon Web Services is growing…don’t ask.

Meanwhile, the rest of IBM’s business, a mix of

consulting and outsourcing, has been fair-to-middling-to-poor.

The reality, we think—never stated on an IBM

call, because the discussion never veers from the numbers, but fairly obvious all the same it would seem—is that much of IBM’s business is tied

to the “higher value, more profitable technologies,” touted in the IBM annual report as the areas towards which the company has been shifting its business mix over the years (think: helping a company install expensive SAP software on big-iron IBM hardware with white-shoe IBM consultants running the show, all financed by IBM) while shedding the stuff Wall Street did not care for (even its baby, the disk drive business, which IBM invented).

call, because the discussion never veers from the numbers, but fairly obvious all the same it would seem—is that much of IBM’s business is tied

to the “higher value, more profitable technologies,” touted in the IBM annual report as the areas towards which the company has been shifting its business mix over the years (think: helping a company install expensive SAP software on big-iron IBM hardware with white-shoe IBM consultants running the show, all financed by IBM) while shedding the stuff Wall Street did not care for (even its baby, the disk drive business, which IBM invented).

And that kind of high cost IT infrastructure business is yesterday’s glory. (Just ask Avon Products, which we will get to in a bit.)

Of course, if you are an IBM shareholder, it has been a great ride. After all, pretty much everything the company has been doing, like the song says, it has been doing for you.

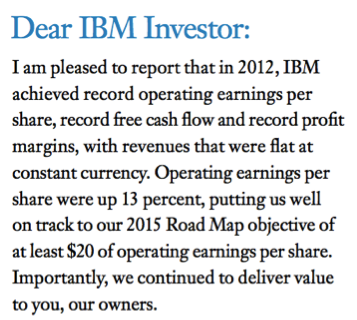

Here, for example, is how last year’s letter

to IBM shareholders began:

to IBM shareholders began:

Notice there is not one mention—not one—of

the company’s customers in that first paragraph.

the company’s customers in that first paragraph.

You think those customers don’t notice?

After reading year after year about how many billions of dollars of IBM stock were purchased by IBM using the hard-earned dollars of those customers ($14 billion in

2013, and $140 billion since 2000), you think that those customers, who weren’t thanked by IBM in that letter or on its earnings calls, don’t wonder how Amazon—purveyor of the very

kind of cloud offering that is allowing companies young and old to get online

without all that expensive, high margin stuff IBM pushes—speaks to its

shareholders?

2013, and $140 billion since 2000), you think that those customers, who weren’t thanked by IBM in that letter or on its earnings calls, don’t wonder how Amazon—purveyor of the very

kind of cloud offering that is allowing companies young and old to get online

without all that expensive, high margin stuff IBM pushes—speaks to its

shareholders?

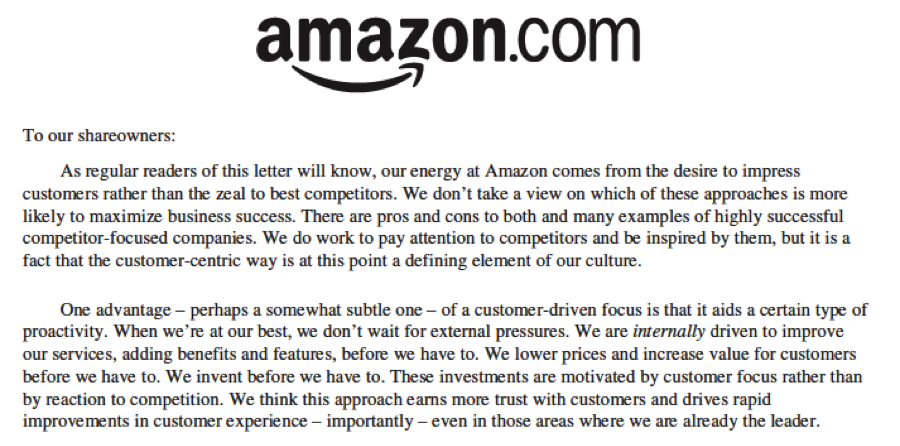

Well here’s how Amazon speaks to its

shareholders:

shareholders:

By our count, Amazon uses the term “customer” twice

in the first paragraph and six times in the first two paragraphs.

And instead of talking about raising gross

margins, operating margins and net income margins, as IBM does in its annual

report, Amazon talks about lowering prices to those customers.

in the first paragraph and six times in the first two paragraphs.

And instead of talking about raising gross

margins, operating margins and net income margins, as IBM does in its annual

report, Amazon talks about lowering prices to those customers.

No wonder just last month Avon Products

jettisoned a $100 million-plus ERP implementation that “did not show a clear

return on investment.” For the record, SAP

was the ERP system, with IBM WebSphere being used to build the “user

interface,” such as it was.

jettisoned a $100 million-plus ERP implementation that “did not show a clear

return on investment.” For the record, SAP

was the ERP system, with IBM WebSphere being used to build the “user

interface,” such as it was.

And that’s exactly the kind of big budget

project IBM’s wheelhouse has been crafted for.

project IBM’s wheelhouse has been crafted for.

And those are exactly the kind of projects that are giving way to the brave new world of Web 2.0.

Perhaps that’s also the reason why every quarter in the last couple years IBM’s revenues seem to be down, or shy of forecasts, or both; and why every

quarter last year IBM’s free cash flow was down year-over-year; and why last October the company revised

its cumulative “Roadmap” cash flow downward from $100 billion to $85 billion; and why the company seems to be trying to jettison any kind of non-sexy business that makes something that plugs into a wall.

quarter last year IBM’s free cash flow was down year-over-year; and why last October the company revised

its cumulative “Roadmap” cash flow downward from $100 billion to $85 billion; and why the company seems to be trying to jettison any kind of non-sexy business that makes something that plugs into a wall.

Of course, just as there are dangers in

analysts leaning too much on management for direction, there are dangers in

managements leaning too much on analysts for direction—like when IBM listened

to everyone telling them to get rid of that dopey old disk drive business.

analysts leaning too much on management for direction, there are dangers in

managements leaning too much on analysts for direction—like when IBM listened

to everyone telling them to get rid of that dopey old disk drive business.

After all, that dopey old disk drive business is now a hot,

hot, hot “cloud” business…the very kind of business IBM wants to brag about on its earnings call.

But not to worry, the $20 EPS Roadmap still stands…with an asterisk, of course.

hot, hot “cloud” business…the very kind of business IBM wants to brag about on its earnings call.

But not to worry, the $20 EPS Roadmap still stands…with an asterisk, of course.

Makes you wonder who’s being manipulated here.

Jeff Matthews

Author “Secrets in Plain

Sight: Business and Investing Secrets of Warren Buffett”

Sight: Business and Investing Secrets of Warren Buffett”

(eBooks on Investing,

2013) $4.99 Kindle Version at

Amazon.com

2013) $4.99 Kindle Version at

Amazon.com

©

2014 NotMakingThisUp, LLC

2014 NotMakingThisUp, LLC

The

content contained in this blog represents only the opinions of Mr.

Matthews. Mr. Matthews also acts as an

advisor and clients advised by Mr. Matthews may hold either long or short

positions in securities of various companies discussed in the blog based upon

Mr. Matthews’ recommendations. This

commentary in no way constitutes investment advice, and should never be relied

on in making an investment decision, ever.

Also, this blog is not a solicitation of business by Mr. Matthews: all inquiries

will be ignored. And if you think Mr.

Matthews is kidding about that, he is not.

The content herein is intended solely for the entertainment of the

reader, and the author.

content contained in this blog represents only the opinions of Mr.

Matthews. Mr. Matthews also acts as an

advisor and clients advised by Mr. Matthews may hold either long or short

positions in securities of various companies discussed in the blog based upon

Mr. Matthews’ recommendations. This

commentary in no way constitutes investment advice, and should never be relied

on in making an investment decision, ever.

Also, this blog is not a solicitation of business by Mr. Matthews: all inquiries

will be ignored. And if you think Mr.

Matthews is kidding about that, he is not.

The content herein is intended solely for the entertainment of the

reader, and the author.