Well the IBM 2013 10K is out, and it kicks off with what can only be described as a

180-degree turn in the way the company presents itself to the public.

180-degree turn in the way the company presents itself to the public.

As we pointed out here and here, IBM has spent

the last five years presenting itself to the public as a

shareholder-friendly—indeed, shareholder-obsessed—dividend-and-buyback machine

that prided itself on jacking up margins (both gross and net) by swapping in

and out of business lines, “rebalancing” its workforce (i.e. layoffs), and avoiding the taxman however (and wherever—e.g.

The Netherlands) the laws allowed it to.

the last five years presenting itself to the public as a

shareholder-friendly—indeed, shareholder-obsessed—dividend-and-buyback machine

that prided itself on jacking up margins (both gross and net) by swapping in

and out of business lines, “rebalancing” its workforce (i.e. layoffs), and avoiding the taxman however (and wherever—e.g.

The Netherlands) the laws allowed it to.

But that was last year.

This

year, it seems, IBM is a new company.

year, it seems, IBM is a new company.

Gone from the “Strategy” declaration in the opening pages of the 2013 10K is the previous year’s braggadocio about “sustained

earnings per share growth and strong cash generation” on the backs of customers

whose main role seemed to be to hand cash to IBM in return for the pleasure of

watching IBM’s stock price rise on the strength of ever-increasing EPS, thanks mainly to share

repurchases from all that cash.

earnings per share growth and strong cash generation” on the backs of customers

whose main role seemed to be to hand cash to IBM in return for the pleasure of

watching IBM’s stock price rise on the strength of ever-increasing EPS, thanks mainly to share

repurchases from all that cash.

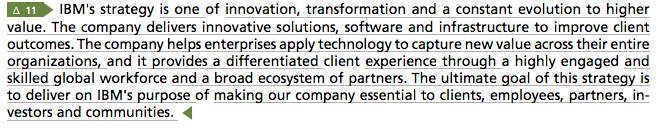

In its place is a new “purpose,” which, we are

told with a straight face, is “making our company essential to clients,

employees, partners, investors and communities.”

told with a straight face, is “making our company essential to clients,

employees, partners, investors and communities.”

(Note to Wall Street: you no longer rank first

on IBM’s list of pals—you now rank fourth.)

on IBM’s list of pals—you now rank fourth.)

Lest readers think we are

making up this 180 turn in the infamous IBM “Roadmap,” we provide below the deletion (in red type) from the “Strategy” discussion in Part 1, Item 1, of IBM’s 2012 10K, followed by its replacement (in green type) in IBM’s newly released 2013 10K. (Both thanks to the indispensable StreetEvents

“Daily Delta” service.)

making up this 180 turn in the infamous IBM “Roadmap,” we provide below the deletion (in red type) from the “Strategy” discussion in Part 1, Item 1, of IBM’s 2012 10K, followed by its replacement (in green type) in IBM’s newly released 2013 10K. (Both thanks to the indispensable StreetEvents

“Daily Delta” service.)

Old IBM:

New IBM:

Meet the new IBM—way different than the old IBM!

Jeff Matthews

Author “Secrets in Plain

Sight: Business and Investing Secrets of Warren Buffett”

Sight: Business and Investing Secrets of Warren Buffett”

(eBooks on Investing,

2013) $4.99 Kindle Version at

Amazon.com

2013) $4.99 Kindle Version at

Amazon.com

©

2014 NotMakingThisUp, LLC

2014 NotMakingThisUp, LLC

The

content contained in this blog represents only the opinions of Mr.

Matthews. Mr. Matthews also acts as an

advisor and clients advised by Mr. Matthews may hold either long or short

positions in securities of various companies discussed in the blog based upon

Mr. Matthews’ recommendations. This

commentary in no way constitutes investment advice, and should never be relied

on in making an investment decision, ever.

Also, this blog is not a solicitation of business by Mr. Matthews: all

inquiries will be ignored. And if you

think Mr. Matthews is kidding about that, he is not. The content herein is intended solely for the

entertainment of the reader, and the author.

content contained in this blog represents only the opinions of Mr.

Matthews. Mr. Matthews also acts as an

advisor and clients advised by Mr. Matthews may hold either long or short

positions in securities of various companies discussed in the blog based upon

Mr. Matthews’ recommendations. This

commentary in no way constitutes investment advice, and should never be relied

on in making an investment decision, ever.

Also, this blog is not a solicitation of business by Mr. Matthews: all

inquiries will be ignored. And if you

think Mr. Matthews is kidding about that, he is not. The content herein is intended solely for the

entertainment of the reader, and the author.